Financially Fit: Why you should be an investor

Disclaimer: The advice provided in the Financially Fit series is general advice only. It has been prepared without taking into account your objectives, financial situation or needs.

There are many reasons why you might want to look into investing opportunities instead of just piling money into a savings or checking account. To help understand a few of those reasons, I talked with Colleen Nolan, a CPA and financial advisor in the LND Group at Robert W. Baird & Co.

Your greatest advantage right now is time.

As Colleen puts it, “The earlier that an individual can begin investing, the more time the investment has to grow. The compounding factor of time in the market is a powerful force. You also have a much greater ability to withstand market volatility by maintaining a longer-term perspective.”

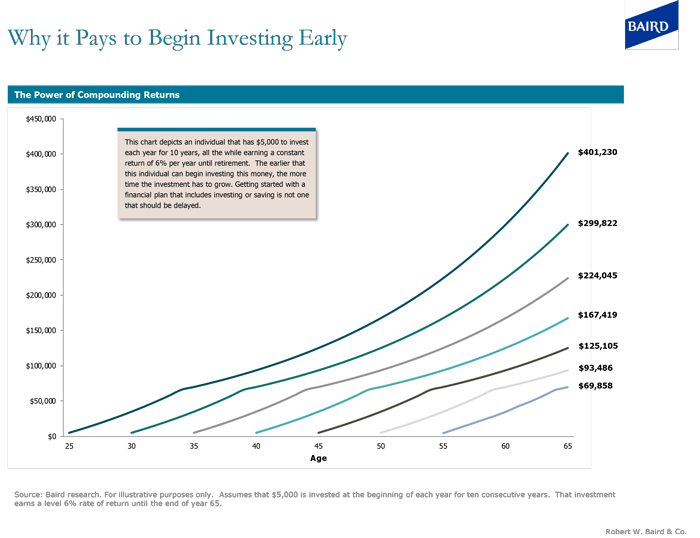

Check out this graph provided by the LND Group and Baird. The amount invested is the same – $5,000 for 10 years ($50,000 total) over different age periods. If you invested that $50,000 from 25-35, it can turn into $400,000+ by the time you are 65. However, if you wait 5 years and start at 30, you will only get around $300,000 – that’s a $100,000 difference – crazy, right?

You give yourself a chance for a higher return potential.

“The advantage of investing money rather than remaining in a savings account is that not only are you giving yourself a chance to grow your asset base, you are also giving your hard earned savings a chance to keep up with economic inflation.” Put another way by Colleen, “If your hard-earned money is sitting in a savings account earning less than 0.5% per year, you are actually losing purchasing power on your savings despite not losing any actual dollars.”

Investments have higher risk. But higher risk often means higher reward.

“Most people have heard of the concept, “no risk, no reward”. While this may be true, and there are certainly risks when it comes to investing, risk in itself can be managed through careful investment planning and diversification. If you invested all of your money into one stock or company, you would be in a very risky position. If the company failed and the stock price fell to zero, you would lose everything you had. However, if you have a well-diversified portfolio comprised of stocks, bonds, mutual funds, and exchange traded funds which are diversified both in size, geography, and industry, you have significantly reduced your risk and can still seek long-term growth.

It’s about having discipline. The market is always going to rise and fall as a healthy economy should be cyclical. Where investors tend to fail is by attempting to time the market’s gains or losses. While ongoing portfolio modifications can be beneficial, large and frequent investment changes are often detrimental.”

The good news here? Women are shown to be great investors over time because we can stick things out for the long-term (patience is a virtue, you guys, just check out the graph provided above) and are not as emotionally attached to our investments (making us more likely to ditch the losers – boys and stocks alike). It’s important to note that it’s often better to not try to beat the market. Be smart. Diversify. Don’t be too quick to change up your investments.

Colleen adds, “There have always been good reasons not to invest, but the market has ultimately moved upward.” In other words, yes there is risk involved – but generally speaking, things will work out in the end.

Investments are best-suited for reaching long-term goals (ahem, retirement) most of us can’t reach just by savings alone.

“The main goal that most people need to achieve is the ability to comfortably fund your retirement. This picture looks different for every individual, but the reality is that with careful planning and by beginning early, you can save for a comfortable retirement, and be able to enjoy other wants and goals throughout your life. Remember, without investing, your savings will not keep up with your ability to purchase goods and services in the market. Therefore, you would have to save exponentially more money to fund your retirement without investing. That is money you could use to fund other aspects of your life such as travel, home purchases, and great gym memberships.”

We’ll dig deeper into investments next time (like, what the hell is an ETF?), but if you have any questions or anything to add on this topic, please let us know in the comments!